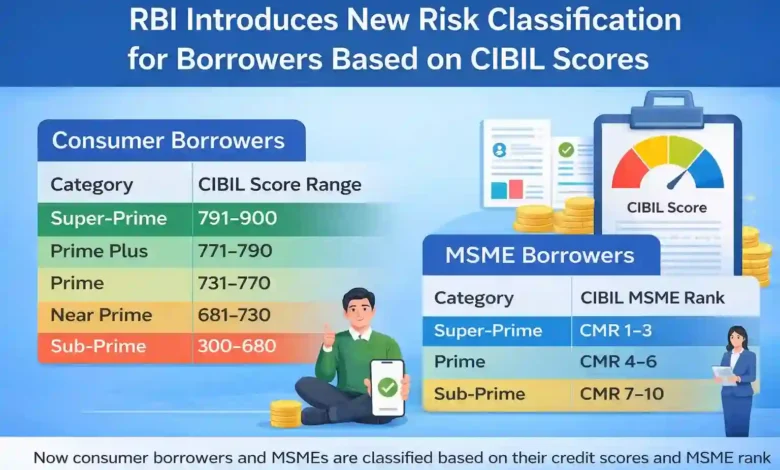

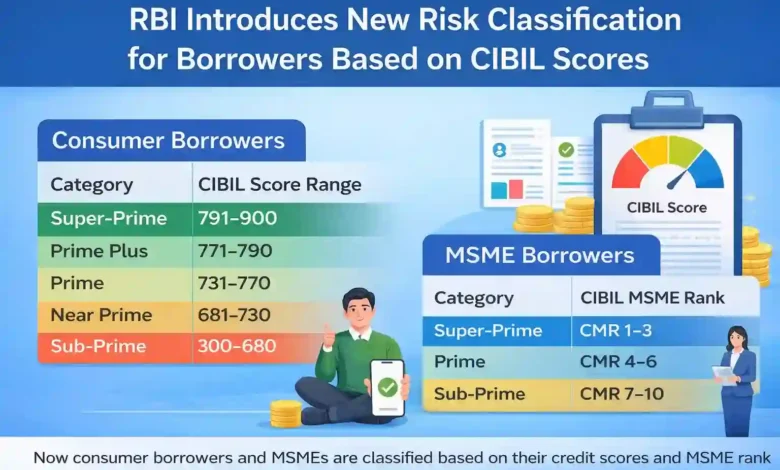

The Reserve Bank of India has introduced a risk-tier classification system for borrowers based on their credit scores. This classification has been explained in the Financial Stability Report (FSR) to help banks and financial institutions assess credit risk more effectively.

The objective of this classification is to improve monitoring of borrowers and strengthen the retail lending system by clearly identifying borrowers based on their creditworthiness.

Risk Classification for Consumer Borrowers

According to the RBI’s framework, consumer borrowers are divided into five categories based on their CIBIL credit score. These categories help banks understand the level of risk associated with lending to a particular borrower.

| Category | CIBIL Score Range |

|---|---|

| Super-Prime | 791 – 900 |

| Prime Plus | 771 – 790 |

| Prime | 731 – 770 |

| Near Prime | 681 – 730 |

| Sub-Prime | 300 – 680 |

Explanation of Categories

- Super-Prime borrowers (791–900) are considered the lowest risk customers with an excellent credit history. Banks prefer lending to such borrowers and usually offer them better interest rates.

- Prime Plus borrowers (771–790) also have a strong credit profile and are considered reliable borrowers.

- Prime borrowers (731–770) fall in the good credit category and generally face no difficulty in obtaining loans.

- Near Prime borrowers (681–730) have moderate credit quality and may face stricter loan conditions.

- Sub-Prime borrowers (300–680) are considered higher-risk borrowers because of weaker credit history or repayment issues.

This classification allows banks to better monitor credit risk across the retail lending ecosystem.

💡 Loan & CIBIL Facts in India

- CIBIL Score Range: In India, credit scores usually range from 300 to 900. A score above 750 is generally considered good for getting loans easily.

- Credit Information Companies: India has four CICs — TransUnion CIBIL, Experian, Equifax and CRIF High Mark.

- Free Credit Report: Every individual in India can get one free credit report every year from each credit bureau.

- Loan Approval: Banks check your CIBIL score, repayment history, income and existing loans before approving a loan.

- Impact of Late Payments: Missing EMIs or credit card payments can reduce your CIBIL score significantly.

- Multiple Loan Applications: Applying for too many loans in a short period can negatively impact your credit score.

Classification for MSME Borrowers

Apart from individual borrowers, RBI has also introduced a risk-tier classification for MSME borrowers based on the CIBIL MSME Rank (CMR). MSME borrowers are categorized into three risk segments:

| Category | CIBIL MSME Rank |

|---|---|

| Super-Prime | CMR 1 – 3 |

| Prime | CMR 4 – 6 |

| Sub-Prime | CMR 7 – 10 |

What These Categories Mean

- Super-Prime MSMEs (CMR 1–3) are considered financially strong and pose low credit risk to banks.

- Prime MSMEs (CMR 4–6) have moderate risk but are generally stable borrowers.

- Sub-Prime MSMEs (CMR 7–10) carry higher risk due to weaker financial or credit performance.

Purpose of the Classification

The RBI has introduced this system to:

- Improve credit risk monitoring

- Standardize borrower assessment across banks

- Strengthen the retail lending ecosystem

- Help banks make better lending decisions based on risk levels

By using CIBIL scores and MSME ranks, banks can quickly determine the financial reliability of borrowers and manage their loan portfolios more effectively.